The Cash-Basis Lie: Why SaaS Founders Fly Blind at $2M ARR

Why managing a SaaS startup on cash-basis accounting is dangerous. Learn how the "February Illusion" hides your burn rate and why ASC 606 compliance

You hit $2M ARR. You have product-market fit. You have a sales team. You have momentum.

You also have a blindfold on.

Most founders at this stage run their business on a cash basis. They look at the bank login screen, see a positive number, and assume the business is healthy. They make hiring decisions based on the checking account balance. They forecast based on cash inflows.

This is not management. This is negligence.

At $2M ARR, cash-basis accounting ceases to be a simplified method for taxes. It becomes a liability. It distorts reality. It feeds you false signals that will eventually drive your company into a wall.

Here is the truth about why your bank balance is lying to you.

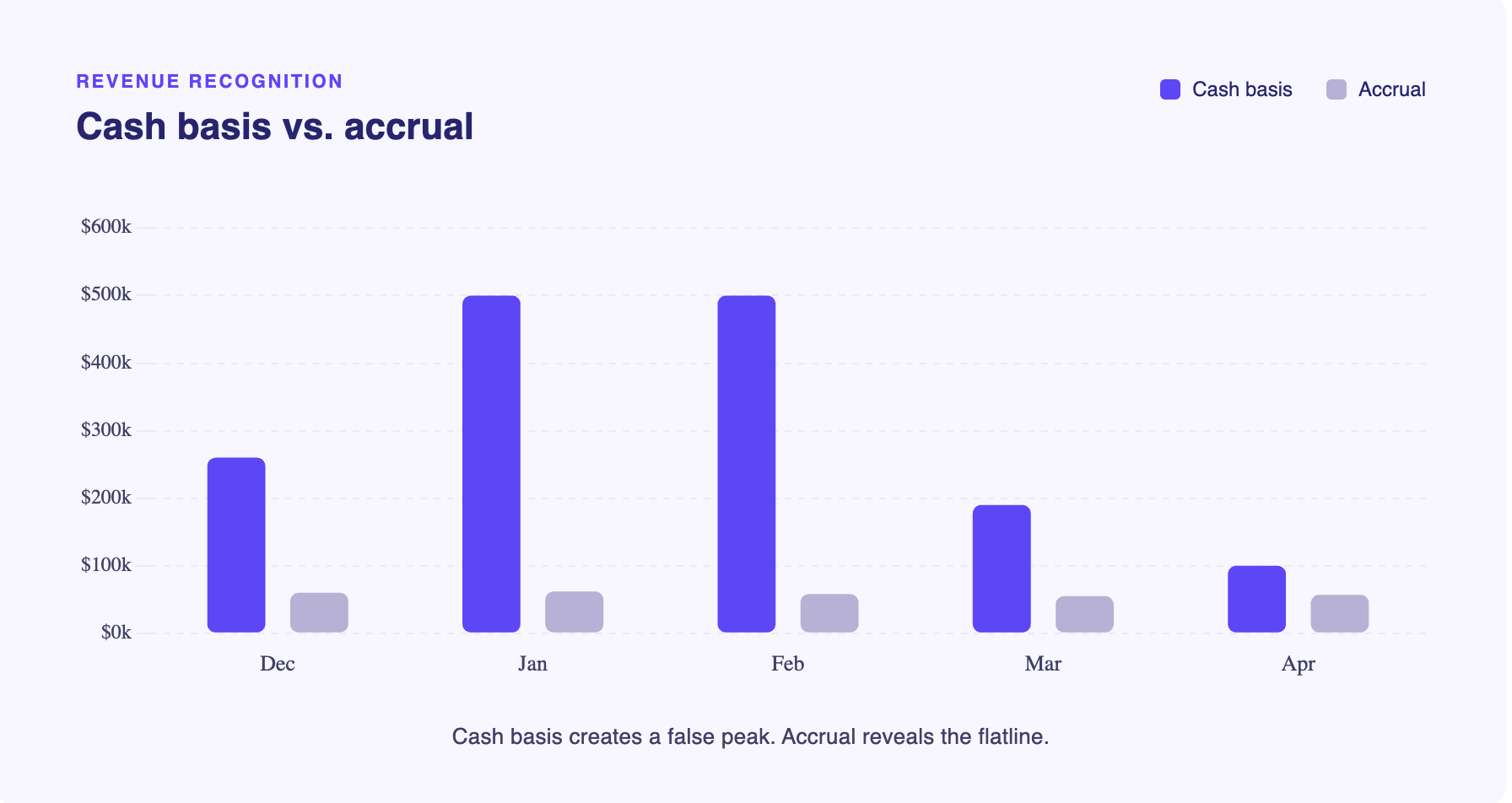

The Symptom: The February Illusion

Cash basis creates a specific, recurring hallucination. We call it the "February Illusion."

You close three major enterprise deals in January. They pay annually upfront. Your bank balance swells. You have $500,000 cash on hand. You feel invincible. You look at that balance and decide to hire two more account executives and a senior engineer.

The P&L looks incredible. You booked $500,000 in revenue in one month against $150,000 in expenses. Net profit: $350,000. You feel like a genius.

Then comes August.

No new enterprise deals close. Churn ticks up slightly. The new hires are expensive. But the cash inflow has stopped. The $500,000 is gone, eaten by six months of burn.

Now your P&L shows $0 revenue and $250,000 in expenses. You are bleeding. You panic. You slash spend. You fire the people you just hired. You damage your employer brand and stall your growth.

You did not suddenly become a bad business in August. You were losing money in February. You just didn't know it.

Cash basis told you that you were rich. It lied.

The Mechanism: The Mismatch of Reality

SaaS economics are distinct. You incur costs monthly (AWS, salaries, rent), but you often receive cash annually.

Cash-basis accounting records revenue when the wire hits. It records expenses when the money leaves. In a subscription model, this creates a total disconnect between effort and reward.

The technical failure here is the violation of the Matching Principle.

If a customer pays you $120,000 upfront for a year of service, you have not earned $120,000 today. You have earned a liability. You owe that customer twelve months of service. You earn that revenue at a rate of $10,000 per month.

Under cash basis, your margins are fiction:

- Month 1: Revenue $120k, Costs $20k. Margin 83%.

- Month 2: Revenue $0, Costs $20k. Margin -100%.

This volatility makes it impossible to calculate CAC, LTV, or Gross Margin accurately. Without these metrics, you cannot engineer growth. You are guessing.

The Monster: The Due Diligence Wall

You might decide to stay on cash basis to save money on bookkeeping. That works until you try to exit or raise Series B.

Institutional investors and acquirers do not read cash-basis books. They require ASC 606 compliance.

When you sign a Letter of Intent (LOI), the acquirer sends in a transaction advisory team. These are auditors. They are hunters. They will ask for your accrual-based financials. You will hand them your cash-basis spreadsheets.

They will stop the process.

They will force you to restate two years of financials. When the numbers are restated, your revenue usually drops. That "record month" you had? Gone. Spread out over the next year. Your EBITDA drops. Your valuation drops with it.

We have seen founders lose millions of dollars in enterprise value during the final week of a deal simply because their accounting was amateur. ASC 606 is not optional. It is the gatekeeper to liquidity.

The Solution: The Financial Engine

Stop viewing accounting as a compliance tax. View Accrual Accounting as a navigation system.

When you switch to accrual, you gain visibility:

- True Gross Margins: You see exactly how much it costs to service a dollar of revenue.

- Cohort Analysis: You see if older customers are becoming more or less profitable over time.

- Deferred Revenue: This is the most important line item on your balance sheet. It represents the cash you have collected but not yet earned.

The Bottom LineYour bank balance tells you how much runway you have today. Accrual accounting tells you if you will be alive next year.

Runway is a countdown clock. Accrual accounting is a compass. Knowing how much time you have left is useless if you are walking in the wrong direction.

If you suspect you are flying blind, apply for a diagnosis.

Subscribe to our newsletter today

Lorem ipsum dolor sit amet consectetur nulla augue arcu pellentesque eget ut libero aliquet ut nibh.